International Travel Insurance Cover Your Essential Guide

International travel insurance coverage is crucial for any trip abroad. It provides a safety net, protecting you against unforeseen circumstances like medical emergencies, trip disruptions, or lost luggage. This guide delves into the intricacies of various policies, covering everything from the scope of coverage to the claims process, helping you choose the perfect policy for your needs.

Understanding the different types of policies, from basic to comprehensive, is key. Factors like destination, trip length, and your age all influence premium costs. This comprehensive overview also examines the claims process, helping you navigate the steps involved in filing a claim. We also discuss specific situations like emergency evacuations and coverages for activities like adventure sports.

Scope of Coverage

International travel insurance provides a crucial safety net for unforeseen events during your trip abroad. It protects you financially against a range of potential issues, from medical emergencies to lost luggage. Understanding the scope of coverage is key to selecting the right policy for your needs.

Comprehensive travel insurance policies offer a broader range of protection than basic policies. This includes coverage for a wider array of potential problems, from medical emergencies to trip cancellations. Choosing the right policy depends on your travel style and planned activities.

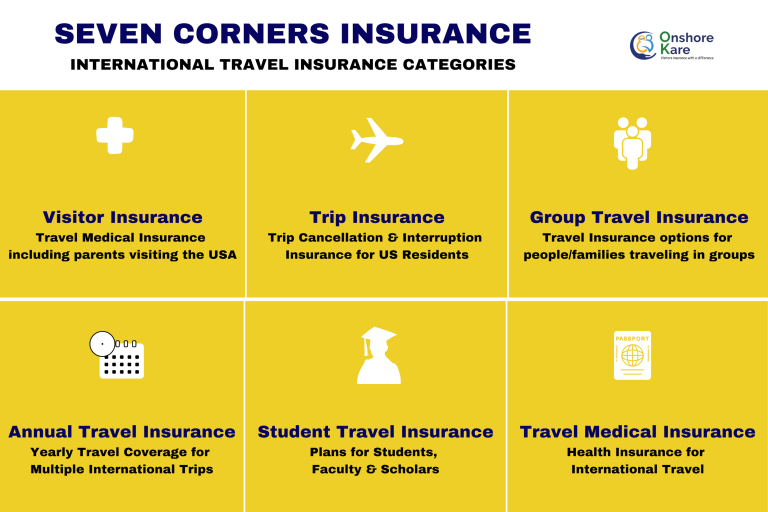

Types of Travel Insurance Policies

Different travel insurance policies cater to varying needs and budgets. Basic policies typically offer essential protection, while comprehensive policies provide more extensive coverage. Adventure travel insurance often includes specialized coverage for extreme activities.

- Basic Policies: These policies provide fundamental coverage for medical emergencies, trip cancellations, and lost or delayed baggage. They are often more affordable, but the level of protection is limited.

- Comprehensive Policies: These policies extend the coverage provided by basic policies, including broader medical expense coverage, trip interruption benefits, and additional baggage protection. They usually offer a more substantial safety net.

- Adventure Travel Insurance: Specifically designed for adventurous travelers, these policies often include enhanced coverage for activities like mountaineering, rock climbing, or whitewater rafting. They may include higher limits for medical expenses and cover potential injuries related to the chosen activities.

Exclusions

Most travel insurance policies have exclusions. These are situations where the policy does not provide coverage. Understanding these exclusions is vital to avoid disappointment. Common exclusions include pre-existing medical conditions, participation in illegal activities, and intentional self-harm. Always carefully review the policy’s terms and conditions.

- Pre-existing Conditions: Many policies exclude coverage for pre-existing medical conditions that manifest during the trip. This often means conditions diagnosed or treated before the policy purchase.

- Illegal Activities: Coverage is often excluded for participation in illegal activities. This includes any activity that violates local laws, including drug use.

- Self-Inflicted Injuries: Policies generally exclude coverage for injuries sustained through intentional self-harm.

Coverage Comparison Table

The following table provides a comparative overview of the coverage offered by different policy types. This allows you to assess the specific protection provided by each type.

| Policy Type | Medical Expenses | Trip Interruption | Baggage Loss | Emergency Evacuation |

|---|---|---|---|---|

| Basic | Limited coverage for emergency medical expenses, often with deductibles and maximum payouts. | Partial coverage for trip interruptions due to unforeseen circumstances, with limitations on the amount reimbursed. | Coverage for lost or damaged baggage, with limitations on the amount and types of items covered. | Limited coverage for emergency evacuation, often with specific conditions and exclusions. |

| Comprehensive | Extensive coverage for medical expenses, including pre-hospital care, hospital stays, and medical evacuations, often with higher maximum payouts. | Comprehensive coverage for trip interruptions, covering costs associated with trip cancellations, rerouting, or delays. | Full coverage for lost or damaged baggage, often covering a wider range of items. | Comprehensive coverage for emergency evacuations, covering transportation, medical care, and associated expenses. |

Factors Affecting Premium: International Travel Insurance Cover

The cost of international travel insurance is not a fixed amount. Several variables influence the premium, ensuring the policy adequately covers the specific risks associated with each trip. Understanding these factors is crucial for travelers to make informed decisions and select appropriate coverage.

The premium amount is a direct reflection of the estimated risk associated with a specific trip. This risk assessment considers a range of factors, each contributing to the overall premium calculation. Factors like destination, trip duration, and the traveler’s profile all play a significant role in determining the final premium.

Destination Impact

Different destinations pose varying levels of risk, impacting the cost of insurance. Countries with higher crime rates, political instability, or significant health concerns typically command higher premiums. Travelers venturing to regions with limited medical infrastructure or those experiencing natural disasters frequently face increased insurance costs.

Trip Duration Impact

The length of a trip directly correlates with the potential for unforeseen circumstances. Longer trips naturally expose travelers to a greater array of potential risks, leading to higher insurance premiums. For example, a three-week backpacking trip across Southeast Asia will likely have a higher premium than a weekend getaway to a nearby city. The extended exposure to diverse situations and potential complications justifies the higher cost.

Traveler’s Age and Health Impact: International travel insurance covers

The age and health status of the traveler are critical considerations in determining the insurance premium. Younger travelers are generally considered higher risk, and thus face potentially higher premiums, due to their perceived higher propensity for unforeseen events, such as accidents or illnesses. Similarly, pre-existing health conditions or chronic illnesses may lead to a higher premium because they increase the likelihood of requiring medical attention during the trip. Consider a traveler with a history of heart conditions; the insurance company will likely assess this as a higher risk and charge a premium accordingly. Similarly, an elderly traveler may require additional coverage for age-related risks, further impacting the premium. Insurers use actuarial data and risk assessments to adjust premiums based on these factors.

Coverage Options Impact

The level of coverage selected significantly affects the premium. A comprehensive policy encompassing medical emergencies, trip cancellations, and baggage loss usually carries a higher premium than a basic policy. The comprehensive policy provides broader protection, and insurers factor this into the premium calculation. For example, an adventure-travel policy that includes coverage for extreme sports will be significantly more expensive than a standard policy for a relaxing vacation. The broader coverage necessitates a higher premium due to the higher risk profile associated with the adventure activities.

Claims Process

Source: mylegaledge.com

Filing a claim with your international travel insurance is a straightforward process designed to assist you in a smooth recovery should the unexpected occur. Understanding the procedure and required documentation will ensure a timely and efficient resolution to your claim. This section details the typical claims process, steps involved, and the necessary documentation.

Typical Claims Process

The claims process for international travel insurance generally involves a series of steps to assess the validity and coverage of your claim. This structured approach ensures a fair and consistent evaluation of each incident. The process often begins with a preliminary review by the insurance provider to confirm the event falls within the scope of your policy.

Steps Involved in Filing a Claim

To initiate the claims process, you need to follow these crucial steps. Prompt action and adherence to the Artikeld procedure are vital for a smooth claim resolution.

- Report the Claim: Contact your insurance provider as soon as possible after the incident. Provide a detailed account of the event, including the date, time, location, and nature of the claim.

- Gather Required Documentation: Collect all necessary documents to support your claim. This may include receipts, medical reports, police reports, travel itineraries, flight confirmations, and any other supporting evidence.

- Submit the Claim Form: Complete the claim form provided by your insurance provider. Ensure you accurately fill out all the required information, including personal details, policy information, and details of the incident.

- Provide Supporting Documents: Submit the collected supporting documentation to the insurance provider. Ensure all documents are clear, legible, and properly organized for easy processing.

- Await Review: Your insurance provider will review the claim and supporting documentation. They may request additional information or clarification. Be prepared to provide any further details or evidence promptly.

- Receive Decision: The insurance provider will notify you of their decision regarding your claim. If the claim is approved, they will provide instructions on how to receive the reimbursement.

Required Documentation

Proper documentation is crucial for a successful claim. The specific documents required may vary depending on the nature of the claim, but some common examples include:

- Medical Records: If the claim involves medical expenses, provide detailed medical reports, bills, and receipts for treatment.

- Police Reports: In cases of theft or other criminal activities, a police report is often necessary to support the claim.

- Travel Documents: Copies of your passport, visa, flight tickets, and travel itinerary can assist in verifying your trip and the circumstances of the claim.

- Receipts: For any expenses incurred, such as medical bills, lost luggage expenses, or emergency evacuation, receipts are essential to substantiate the claim.

Contacting the Insurance Provider

Contacting your insurance provider is a critical part of the claims process. Having clear communication channels ensures a smooth and efficient resolution.

- Phone: Use the phone number provided on your policy documents to reach a claims representative.

- Email: Use the designated email address on your policy documents for correspondence.

- Online Portal: Many insurance providers offer online portals for managing claims, which may include submitting forms and tracking progress.

Step-by-Step Guide for Making a Claim

This step-by-step guide provides a concise overview of the claim process.

- Report the incident to the insurance provider immediately.

- Gather all necessary documents, including medical records, receipts, and police reports.

- Complete the claim form accurately and submit it with supporting documentation.

- Keep detailed records of all communication with the insurance provider.

- Follow up with the insurance provider regularly to track the progress of your claim.

Choosing the Right Policy

Selecting the appropriate international travel insurance policy is crucial for a smooth and worry-free trip. Understanding the nuances of different policies, carefully evaluating coverage details, and considering customer feedback are essential steps in making an informed decision. This process ensures you’re adequately protected against unforeseen circumstances while traveling abroad.

Key Criteria for Policy Selection

Several key criteria significantly impact the suitability of a travel insurance policy. These factors should be thoroughly considered before making a purchase. A comprehensive understanding of these aspects helps ensure you choose a policy that aligns with your specific travel needs and budget.

- Policy Terms and Conditions: Carefully review the policy’s terms and conditions. This document articulates the specific circumstances covered and excluded. Understanding the policy’s exclusions is vital, as it helps avoid surprises during a claim. For example, pre-existing medical conditions might be excluded or have specific limitations. A comprehensive understanding of the policy’s scope of coverage, including its limitations and exclusions, will empower you to make an informed decision.

- Coverage Limits: Assess the coverage limits for various potential claims, such as medical expenses, lost luggage, trip cancellations, and emergency evacuation. Consider the maximum amount the policy will pay for each eventuality. The coverage limits should adequately address the potential financial implications of various travel-related risks. For example, a policy with low medical expense coverage might not be sufficient for extensive treatment abroad.

- Customer Reviews: Leverage online customer reviews to gain insights into the experiences of previous policyholders. Look for patterns in the reviews to understand the insurer’s reputation in handling claims and providing customer service. Reviewing customer feedback helps in evaluating the reliability and responsiveness of the insurance provider.

Comparing Policies

Comparing policies effectively is essential to finding the best option for your needs. A methodical comparison process, focusing on key aspects, ensures you make an informed choice.

- Systematic Comparison: Develop a structured approach to comparing different policies. Use a spreadsheet or a dedicated comparison tool to list key features, coverage limits, and costs. Comparing policies in a structured manner facilitates a thorough evaluation and minimizes overlooking important details. For instance, organize your comparisons by identifying coverage areas, coverage amounts, and associated costs.

- Seek Professional Advice: Consult with a travel agent or financial advisor for guidance on selecting the most suitable policy. Their expertise can help you navigate the complexities of different policies and identify the best fit for your individual needs. This could save time and effort in the comparison process.

- Transparency and Clarity: Ensure the policy’s terms and conditions are presented clearly and concisely. Avoid policies with vague or ambiguous wording. Understanding the policy’s language and its coverage provisions is essential to avoid potential misunderstandings during the claim process.

Policy Provider Comparison Table

The table below illustrates a comparison of different policy providers, highlighting their coverage limits, customer reviews, and policy terms. This table provides a concise overview of the key differences between insurance providers.

| Provider | Coverage Limits (USD) | Customer Reviews (Average Rating) | Policy Terms (e.g., Pre-existing Conditions) |

|---|---|---|---|

| Company A | Medical Expenses: 100,000; Trip Cancellation: 5,000; Baggage Loss: 1,000 | 4.5/5 (Based on 100+ reviews) | Pre-existing conditions are excluded after 30 days of diagnosis. |

| Company B | Medical Expenses: 150,000; Trip Cancellation: 10,000; Baggage Loss: 2,000 | 4.2/5 (Based on 50+ reviews) | Pre-existing conditions are covered if declared and accepted. |

| Company C | Medical Expenses: 75,000; Trip Cancellation: 3,000; Baggage Loss: 500 | 3.8/5 (Based on 25+ reviews) | Pre-existing conditions not covered. |

Emergency Situations

International travel insurance plays a crucial role in mitigating unforeseen circumstances during your journey. This section details the types of emergencies covered and how the insurance can support you in such situations. Understanding your coverage is vital for peace of mind while traveling abroad.

Emergencies can range from minor illnesses to life-threatening events. Your policy’s scope defines the specific situations it addresses, and the level of support offered. The coverage extends beyond simply paying for medical expenses; it often encompasses crucial services like repatriation and medical evacuation.

Covered Emergency Situations

This section articulates the typical range of emergencies covered by international travel insurance. Policies generally include provisions for a broad spectrum of medical emergencies, including but not limited to:

- Medical Emergencies: This covers unforeseen illnesses or injuries requiring immediate medical attention. Examples include sudden onset of severe conditions like appendicitis, heart attacks, or strokes, or accidents like fractures sustained during an outdoor activity. Emergency medical care at hospitals, surgeries, and the use of specialist care are generally included in the coverage.

- Repatriation: In case of a serious medical emergency or unforeseen circumstances requiring urgent return to your home country, repatriation services might be provided. This includes the necessary arrangements for air or other transportation to get you home.

- Medical Evacuation: If medical treatment in the destination country is insufficient, the policy may cover the cost of evacuating you to a more appropriate facility in another country. This could be necessary due to the unavailability of specialized care or if the local medical infrastructure cannot meet the immediate needs.

- Emergency Dental Treatment: Some policies include coverage for unforeseen dental emergencies, which may be particularly important for prolonged trips.

- Lost or Stolen Passport/Travel Documents: This coverage is designed to assist in regaining lost or stolen travel documents to allow continued travel and repatriation.

Examples of Emergency Situations

To illustrate the practical application of emergency coverage, consider these examples:

- A traveler experiencing a severe allergic reaction during a trip requires immediate medical attention and hospitalization. The policy’s medical expense coverage would assist in paying for treatment and potential repatriation.

- A traveler suffers a serious injury during a hiking excursion in a remote area. The policy’s medical evacuation coverage could help in transporting the traveler to a hospital with better facilities.

- A traveler’s passport is stolen. The insurance coverage may assist in obtaining a temporary passport and arranging return travel.

Insurance Role in Repatriation or Medical Evacuation

The role of insurance in repatriation or medical evacuation is significant, as it manages the logistical and financial aspects of a potentially complex situation. The insurance company handles:

- Coordination: Contacting medical professionals, arranging transportation, and coordinating with local authorities to facilitate a smooth evacuation process.

- Financial Support: Covering the costs associated with repatriation or medical evacuation, including transportation, medical fees, and other necessary expenses.

- Finding Appropriate Facilities: Identifying suitable medical facilities in another country that can provide the necessary treatment for the injured person.

Summary of Common Emergency Situations and Insurance Response

| Emergency Situation | Insurance Response |

|---|---|

| Serious illness or injury requiring hospitalization | Coverage for medical expenses, potential repatriation |

| Accident requiring medical evacuation | Coverage for evacuation to a suitable medical facility |

| Lost or stolen travel documents | Assistance in obtaining replacements and facilitating continued travel |

Coverage for Specific Activities

Travel insurance policies typically offer standard coverage for a wide range of activities, but certain activities demand additional or specialized protection. This section includes articles specific activities requiring supplemental coverage and the process for obtaining it.

Understanding the limitations of standard coverage is crucial for ensuring adequate protection during your trip. Specific activities like adventure sports, extreme sports, or travel to remote locations might require specialized coverages that go beyond the typical inclusions.

Identifying Activities Requiring Additional Coverage

A comprehensive travel insurance policy often includes standard coverage for typical travel scenarios. However, some activities inherently carry greater risks, necessitating specific protections. Activities demanding specialized coverage typically fall into the following categories:

- Adventure Sports:

- Extreme Sports:

- Travel to Remote or Hazardous Locations:

Adventure Sports Coverage

Adventure sports, such as rock climbing, whitewater rafting, and mountain biking, often involve a higher degree of risk than everyday activities. To obtain adequate protection, travelers should inquire about add-on adventure sports packages or seek coverage through specialized adventure travel insurance. These policies often address inherent risks and specific medical expenses associated with these activities.

Extreme Sports Coverage

Extreme sports, like skydiving, paragliding, or BASE jumping, carry significantly elevated risks. Specific insurance policies tailored to these high-risk activities are usually necessary. These policies often have increased coverage limits for medical expenses, and in some cases, may also cover potential property damage.

Coverage for Specific Locations

Some destinations pose unique risks, like remote areas with limited medical facilities. Insurance providers often offer coverage tailored to the specific location’s hazards. This type of coverage typically addresses emergency medical evacuation, potentially more extensive medical care, or alternative transportation options. These provisions might include specific stipulations for certain destinations known for challenging conditions or limited accessibility.

Examples of Activities Outside Standard Coverage

Standard travel insurance policies typically do not cover activities with substantial inherent risks, including:

- Participation in organized military or paramilitary exercises.

- Activities involving the use of hazardous materials.

- Certain forms of extreme sports, unless specifically articulated in the policy.

- Professional athletic events where the participant is compensated for their performance.

Acquiring Additional Coverage for Specific Activities

When considering activities requiring additional coverage, it’s essential to consult the insurance provider directly. They can assess the specific risks associated with the activity and recommend suitable supplemental coverages. Examples of such activities include scuba diving, trekking, or bungee jumping.

- Scuba Diving: To ensure coverage for scuba diving, review the policy’s details carefully, as standard policies often have limitations. Inquire about specific add-ons for scuba diving or specialized policies tailored to water activities. Some policies might require a statement confirming the certification level of the diver.

- Trekking: For trekking expeditions, specialized coverage may be required, depending on the location and the complexity of the trek. Policies should explicitly address the potential for altitude sickness, emergency medical evacuation, and transportation in remote areas.

Policy Documents

Your travel insurance policy is a crucial document outlining the terms and conditions of your coverage. Understanding its contents is essential to ensure you are fully aware of your rights and responsibilities. This section delves into the key elements of a policy document, empowering you to make informed decisions about your coverage.

Essential Documents Included

A comprehensive travel insurance policy typically includes several essential documents, each playing a specific role in defining your coverage. These documents detail your benefits, exclusions, and the procedures to follow in case of an unforeseen event.

-

- Policy Summary/Certificate of Insurance:

This document provides a concise overview of your coverage, outlining the key features and benefits. It’s a quick reference point to grasp the overall protection you’ve secured. This is often the first document you receive.

-

- Policy Wordings/Main Policy Document:

This is the core document that elaborates on the detailed terms and conditions, including specific coverage amounts, exclusions, and procedures for making claims.

-

- Endorsements/Amendments:

If there are specific additions or modifications to your standard policy, these are detailed in separate endorsements. These might include additional coverage for specific activities or circumstances.

Sections within the Policy

The policy document itself is organized into distinct sections, each providing crucial information about the coverage. Understanding these sections is vital for navigating the document and grasping your protection.

| Section | Description |

|---|---|

| Declaration Page | This page typically includes your personal information, travel details, policy period, and insured amount. |

| Definitions | Provides precise definitions of terms used throughout the policy, ensuring a common understanding. For example, “Emergency Medical Expenses” or “Loss of Passport.” |

| Coverage Summary | A concise overview of the types of coverages provided, including emergency medical, trip cancellation, baggage loss, and more. |

| Conditions | Articles the terms and conditions, responsibilities of the insured, and limitations of the policy. This is often where exclusions are detailed. |

| Exclusions | Lists the circumstances where the policy will not provide coverage. Examples include pre-existing medical conditions or intentional acts. |

| Claims Procedure | Details the steps required to file a claim, including necessary documentation and contact information. |

| Policy Limitations | Specifies any limitations on coverage, such as maximum payout amounts or geographical restrictions. |

Importance of Understanding Terms and Conditions

Thoroughly reviewing the terms and conditions is paramount. This ensures you understand the specifics of your coverage, potential limitations, and exclusions. Misinterpreting these aspects can lead to disappointment if a claim is denied due to a lack of understanding.

“Carefully read and understand every section of the policy document before you travel.”

Visual Representation of a Policy Document

(Note: A visual representation of a policy document cannot be displayed here. A real-world policy document would include the sections described above in a structured format.)

Benefits and Drawbacks

International travel insurance can provide peace of mind during your adventures abroad. It protects you against unforeseen events that can disrupt your trip or lead to significant financial burdens. However, it’s crucial to understand both the advantages and potential limitations to make an informed decision. This section examines the pros and cons of purchasing travel insurance.

Benefits of International Travel Insurance

Travel insurance offers numerous benefits, safeguarding your financial well-being and allowing you to enjoy your trip without undue stress. These benefits are especially important for unforeseen events or emergencies that could disrupt travel plans.

- Financial Protection: Travel insurance can reimburse you for medical expenses, lost luggage, trip cancellations, or delays, reducing the financial impact of unexpected events. For example, a sudden illness abroad requiring hospitalization can quickly drain your funds. Travel insurance can alleviate this burden by covering medical expenses and providing a financial safety net.

- Medical Emergencies: Insurance can cover the high cost of medical treatment in foreign countries, which can be substantially more expensive than in your home country. This is particularly important for pre-existing conditions that may not be covered by your domestic healthcare system. A policyholder requiring extensive medical treatment in a foreign country without insurance would face considerable financial hardship, whereas a policy with comprehensive coverage can mitigate these expenses.

- Trip Interruptions: Unexpected events, like natural disasters or family emergencies, can force you to cancel or cut short your trip. Travel insurance can help reimburse trip costs for cancellations or interruptions. For instance, a policyholder planning a trip to a hurricane-affected region might cancel their trip, and insurance can refund some or all of the expenses. Policies often cover certain disruptions, providing some financial protection in such circumstances.

- Lost or Damaged Luggage: A common concern for travelers is lost or damaged luggage. Travel insurance can cover the replacement of lost or damaged items, including essential travel documents. This is crucial for maintaining continuity during a trip and for recovering from unforeseen circumstances.

Drawbacks and Limitations of Travel Insurance

While travel insurance offers substantial benefits, it’s important to acknowledge its limitations. Policies often exclude certain activities or events, and the coverage may not be comprehensive in all situations.

- Exclusions and Limitations: Travel insurance policies typically exclude coverage for pre-existing medical conditions, certain types of sports, or activities deemed high-risk. The specific exclusions can vary widely between providers, so careful review of the policy document is crucial. A policyholder with a pre-existing heart condition may be excluded from coverage in the case of a heart attack while traveling.

- Limited Coverage for Certain Activities: Some activities, such as extreme sports or risky travel to specific regions, might not be covered by the standard policy. Insurance companies typically set limits to protect themselves from excessive claims related to dangerous activities.

- Claims Process Complexity: Filing a claim can sometimes be a lengthy and complicated process, requiring extensive documentation and communication with the insurance company. This is something to consider as part of the total cost of purchasing travel insurance. The claims process may vary, and understanding the procedures in advance can save time and frustration.

- Cost and Value: The cost of travel insurance can vary significantly based on the trip duration, destination, and type of coverage. The policyholder needs to consider the cost versus the value of the coverage and if the cost is justified by the potential risks.

Case Studies

Real-world examples can illustrate the positive and negative aspects of travel insurance. These cases demonstrate how policies can provide significant protection or how limitations can lead to disappointment.

- Positive Case: A family traveling to Southeast Asia experienced a sudden illness requiring extensive medical care. Their travel insurance covered the medical expenses, significantly easing their financial burden. This example highlights the value of travel insurance when unforeseen medical emergencies occur.

- Negative Case: A traveler attempted to file a claim for a lost item, but the item was not listed as covered under their policy. This example illustrates the importance of thoroughly reviewing the policy document before purchasing insurance. A policyholder who does not understand the limitations of their policy could be disappointed when filing a claim.

Comparison of Advantages and Disadvantages

A careful comparison of the advantages and disadvantages can help you make an informed decision about purchasing travel insurance.

| Advantages | Disadvantages |

|---|---|

| Financial protection against unexpected events | Exclusions and limitations that may not cover all situations |

| Coverage for medical emergencies | Potential complexity of the claims process |

| Reimbursement for trip interruptions | Varied costs depending on the policy and trip |

| Protection against lost or damaged luggage | Limited coverage for certain activities or destinations |

Outcome Summary

In conclusion, international travel insurance coverage is a vital investment for any traveler. By carefully considering the different policy types, premium factors, and the claims process, you can choose the right insurance to suit your needs and budget. Remember to consider coverage limits, policy terms, and customer reviews when comparing providers. This guide has provided the tools you need to make an informed decision, ensuring your journey abroad is worry-free and protected.